How Do You Know Which Order to List Accounts on a Trial Balance

Analyzing and Recording Transactions

17 Ready a Trial Balance

One time all the monthly transactions have been analyzed, journalized, and posted on a continuous 24-hour interval-to-day basis over the bookkeeping period (a calendar month in our example), we are ready to offset working on preparing a trial balance (unadjusted). Preparing an unadjusted trial remainder is the fourth footstep in the accounting cycle. A trial balance is a list of all accounts in the full general ledger that accept nonzero balances. A trial balance is an important step in the bookkeeping procedure, because it helps identify any computational errors throughout the first 3 steps in the cycle.

Note that for this step, nosotros are considering our trial residual to be unadjusted. The unadjusted trial balance in this section includes accounts earlier they have been adapted. As you lot encounter in pace half dozen of the accounting cycle, nosotros create some other trial balance that is adjusted (see The Adjustment Process).

When constructing a trial remainder, we must consider a few formatting rules, akin to those requirements for financial statements:

- The header must comprise the name of the company, the label of a Trial Balance (Unadjusted), and the engagement.

- Accounts are listed in the bookkeeping equation guild with assets listed first followed by liabilities and finally equity.

- Amounts at the peak of each debit and credit column should have a dollar sign.

- When amounts are added, the final figure in each cavalcade should exist underscored.

- The totals at the stop of the trial balance need to have dollar signs and exist double-underscored.

Transferring information from T-accounts to the trial remainder requires consideration of the final balance in each business relationship. If the concluding balance in the ledger business relationship (T-account) is a debit balance, you will record the total in the left column of the trial balance. If the final residue in the ledger business relationship (T-account) is a credit remainder, you will record the total in the right column.

One time all ledger accounts and their balances are recorded, the debit and credit columns on the trial remainder are totaled to see if the figures in each column match each other. The final total in the debit column must be the same dollar amount that is adamant in the final credit column. For example, if y'all decide that the final debit balance is $24,000 and so the terminal credit residual in the trial balance must likewise exist $24,000. If the two balances are non equal, at that place is a mistake in at least i of the columns.

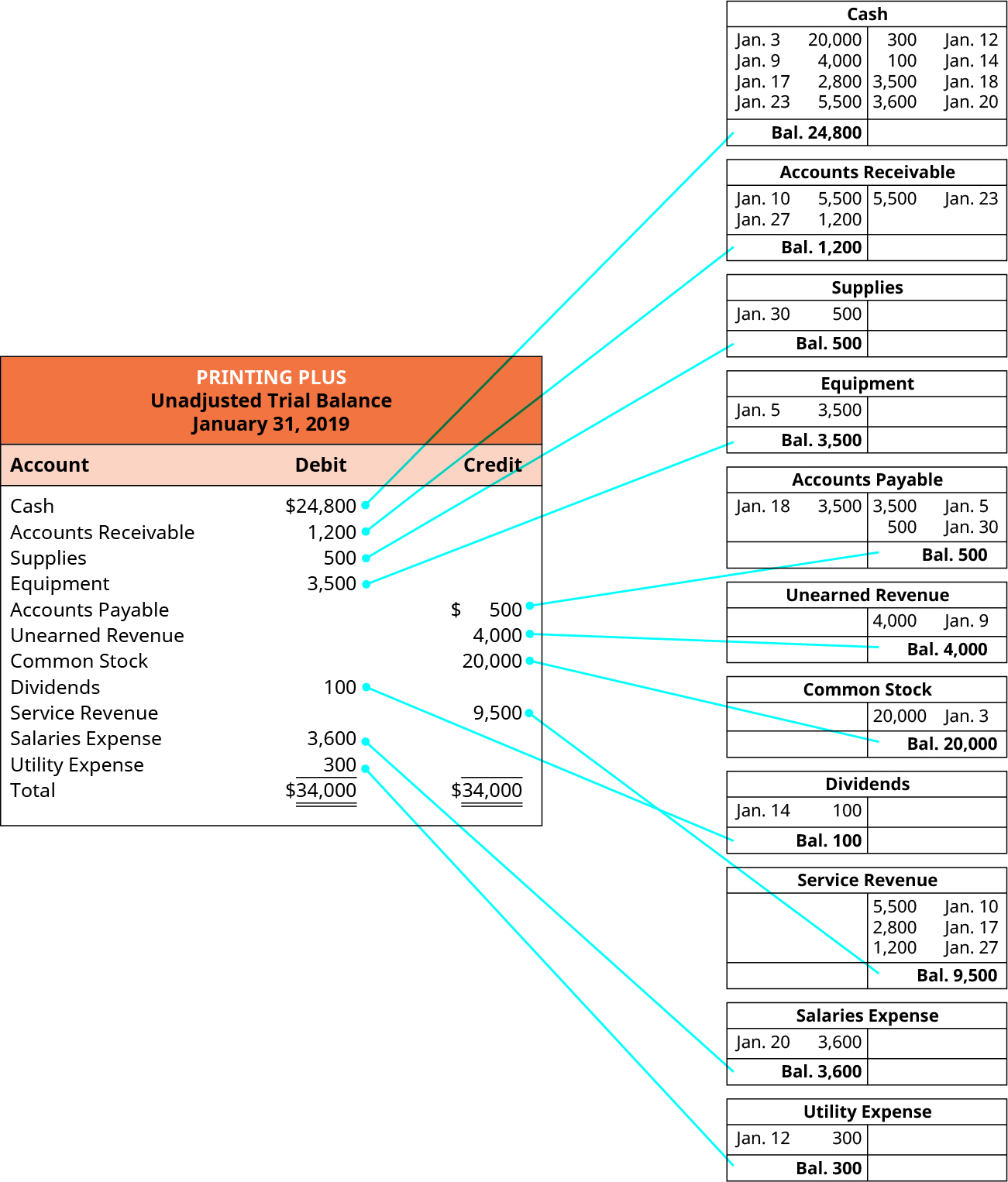

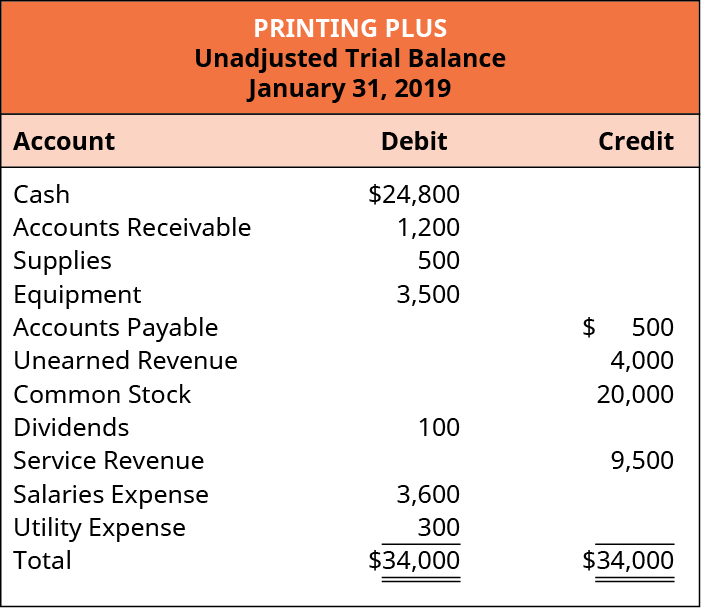

Permit'southward now take a await at the T-accounts and unadjusted trial residual for Printing Plus to see how the information is transferred from the T-accounts to the unadjusted trial balance.

For example, Cash has a final balance of $24,800 on the debit side. This residuum is transferred to the Cash business relationship in the debit column on the unadjusted trial balance. Accounts Receivable ($one,200), Supplies ($500), Equipment ($3,500), Dividends ($100), Salaries Expense ($3,600), and Utility Expense ($300) as well have debit concluding balances in their T-accounts, and so this information will be transferred to the debit column on the unadjusted trial balance. Accounts Payable ($500), Unearned Revenue ($4,000), Common Stock ($20,000) and Service Revenue ($9,500) all have credit terminal balances in their T-accounts. These credit balances would transfer to the credit column on the unadjusted trial residual.

One time all balances are transferred to the unadjusted trial balance, we volition sum each of the debit and credit columns. The debit and credit columns both total $34,000, which ways they are equal and in residue. However, only considering the column totals are equal and in residual, we are still not guaranteed that a error is non present.

What happens if the columns are not equal?

Enron and Arthur Andersen

Ane of the nigh well-known fiscal schemes is that involving the companies Enron Corporation and Arthur Andersen. Enron defrauded thousands by intentionally inflating revenues that did non exist. Arthur Andersen was the auditing firm in charge of independently verifying the accurateness of Enron'southward financial statements and disclosures. This meant they would review statements to make sure they aligned with GAAP principles, assumptions, and concepts, among other things.

It has been declared that Arthur Andersen was negligent in its dealings with Enron and contributed to the collapse of the visitor. Arthur Andersen was brought up on a accuse of obstruction of justice for shredding important documents related to criminal actions past Enron. They were constitute guilty simply had that conviction overturned. Nevertheless, the damage was done, and the company'southward reputation prevented it from operating equally it had.1

Locating Errors

Sometimes errors may occur in the bookkeeping procedure, and the trial remainder can make those errors apparent when information technology does not rest.

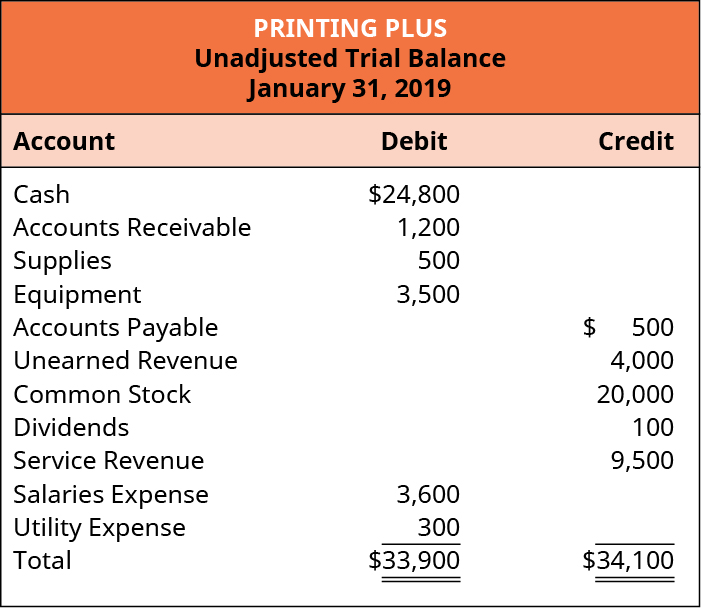

I way to discover the error is to take the difference between the two totals and divide the departure by two. For example, let'due south assume the following is the trial balance for Press Plus.

You observe that the balances are not the same. Find the difference between the two totals: $34,100 – $33,900 = $200 difference. Now carve up the difference by 2: $200/2 = $100. Since the credit side has a higher total, look advisedly at the numbers on the credit side to encounter if whatsoever of them are $100. The Dividends account has a $100 figure listed in the credit column. Dividends unremarkably have a debit balance, just here it is a credit. Look back at the Dividends T-account to encounter if information technology was copied onto the trial residual incorrectly. If the answer is the same as the T-account, then trace it back to the periodical entry to cheque for mistakes. Y'all may discover in your investigation that you copied the number from the T-account incorrectly. Gear up your error, and the debit total volition go up $100 and the credit full downwards $100 and so that they volition both at present be $34,000.

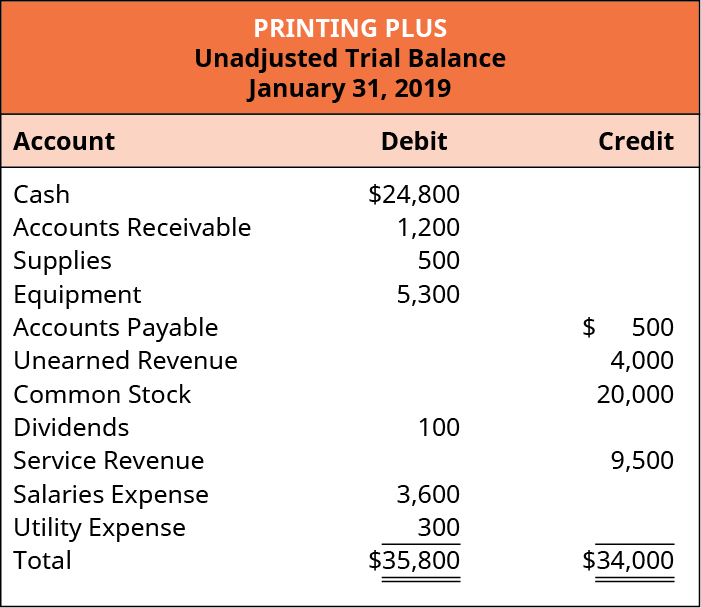

Another way to find an mistake is to have the departure betwixt the two totals and divide by ix. If the outcome of the difference is a whole number, and then you may accept transposed a effigy. For instance, allow's presume the following is the trial balance for Printing Plus.

Find the departure between the two totals: $35,800 – 34,000 = $1,800 difference. This difference divided by nine is $200 ($1,800/nine = $200). Looking at the debit column, which has the higher total, we determine that the Equipment business relationship had transposed figures. The business relationship should be $3,500 and non $5,300. We transposed the three and the five.

What do you do if yous have tried both methods and neither has worked? Unfortunately, you will take to go dorsum through 1 step at a time until you find the fault.

If a trial residual is in residuum, does this mean that all of the numbers are correct? Non necessarily. We can have errors and even so be mathematically in balance. It is of import to go through each stride very advisedly and recheck your work often to avert mistakes early on in the process.

After the unadjusted trial balance is prepared and it appears error-free, a company might wait at its financial statements to get an idea of the company'due south position before adjustments are fabricated to certain accounts. A more than complete picture of visitor position develops after adjustments occur, and an adjusted trial residue has been prepared. These next steps in the bookkeeping cycle are covered in The Adjustment Process.

Completing a Trial Balance

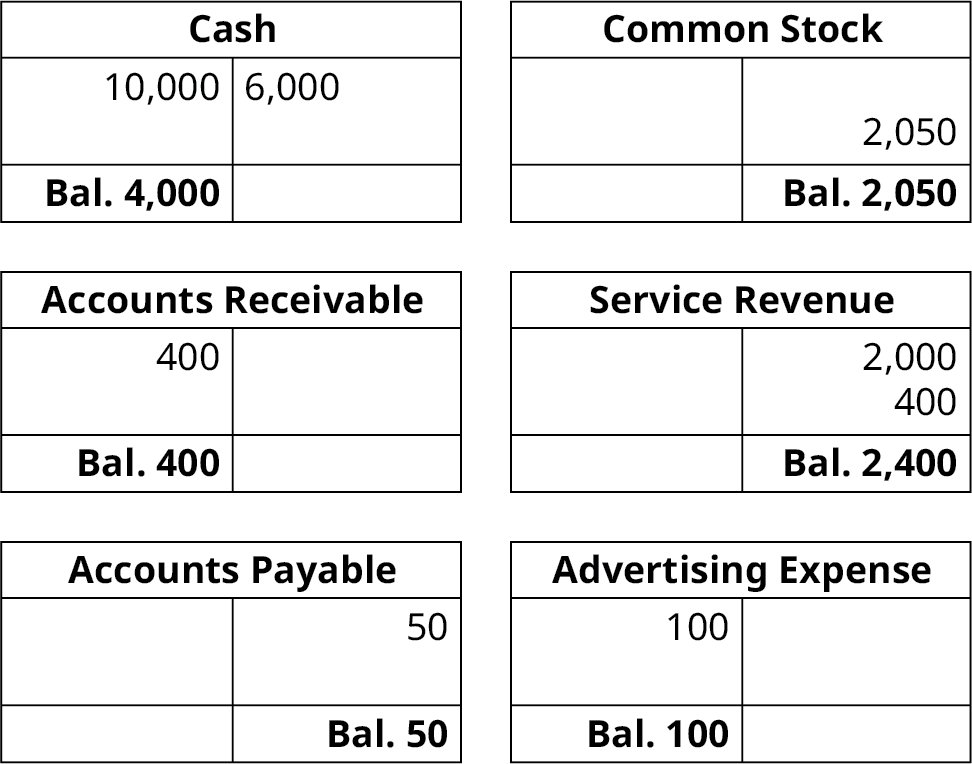

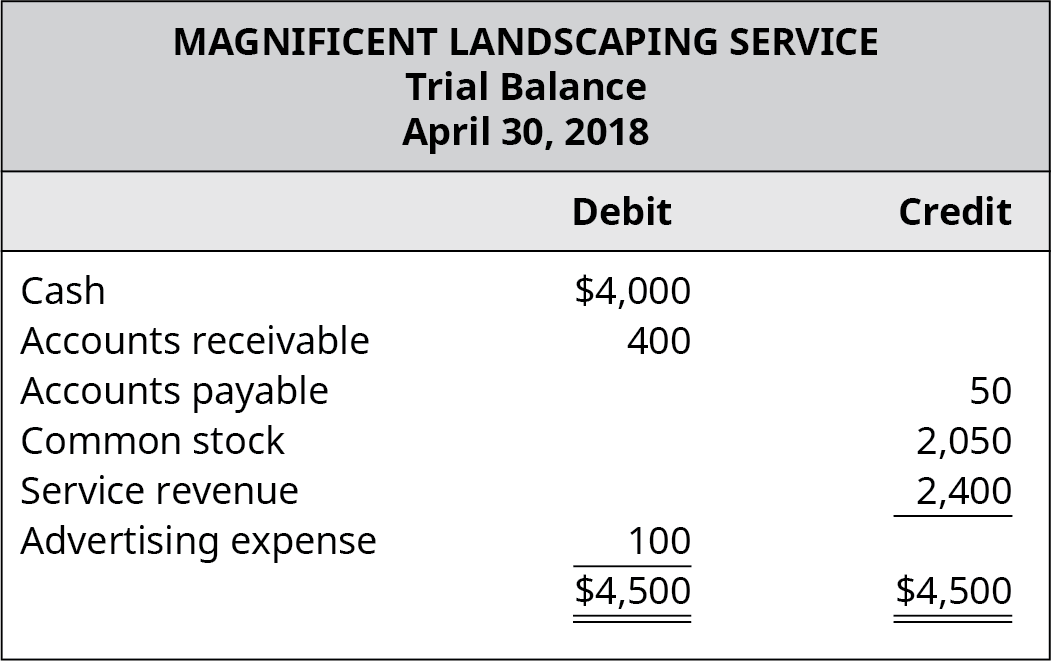

Complete the trial balance for Magnificent Landscaping Service using the post-obit T-account terminal balance information for April 30, 2018.

Solution

Correcting Errors in the Trial Balance

You ain a pocket-sized consulting business. Each month, you gear up a trial balance showing your company's position. After preparing your trial remainder this month, yous discover that it does not residual. The debit column shows $2,000 more dollars than the credit column. You lot decide to investigate this error.

What methods could you use to find the error? What are the ramifications if you do not find and fix this error? How can y'all minimize these types of errors in the futurity?

Fundamental Concepts and Summary

- The trial residuum contains a listing of all accounts in the general ledger with nonzero balances. Data is transferred from the T-accounts to the trial balance.

- Sometimes errors occur on the trial residuum, and there are ways to discover these errors. One may take to get through each step of the accounting process to locate an error on the trial balance.

Exercise Set A

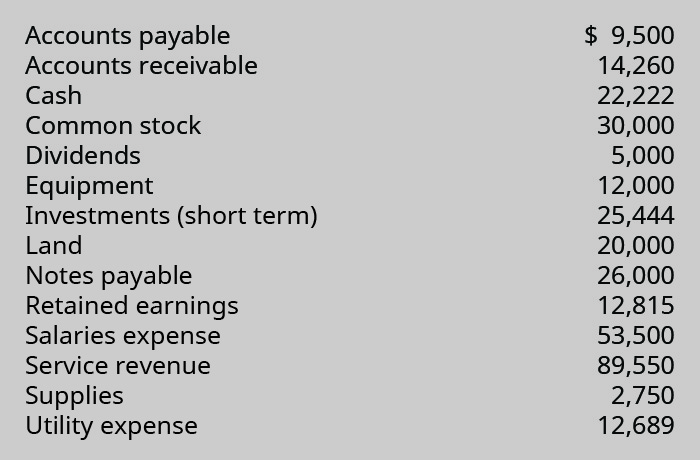

(Figure)Prepare an unadjusted trial balance, in correct format, from the alphabetized account information equally follows. Assume all accounts have normal balances.

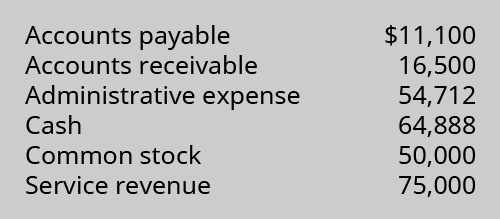

Exercise Set B

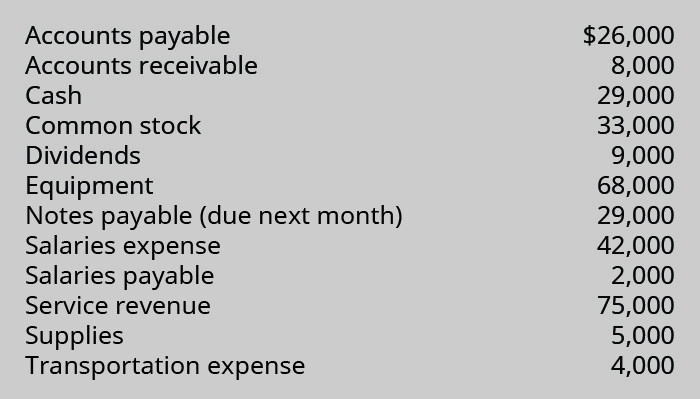

(Figure)Prepare an unadjusted trial balance, in right format, from the alphabetized business relationship information equally follows. Assume all accounts have normal balances.

Problem Set A

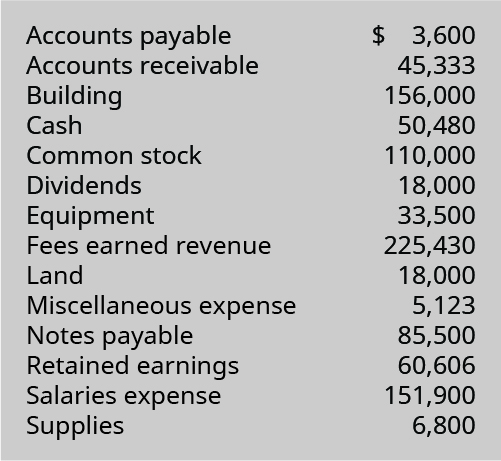

(Effigy)Set an unadjusted trial rest, in correct format, from the following alphabetized account information. Assume accounts have normal balances.

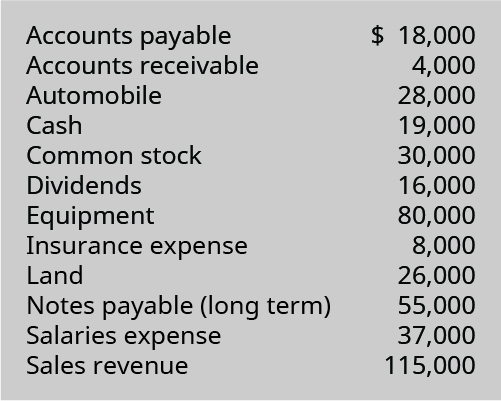

(Figure)Prepare an unadjusted trial balance, in correct format, from the following alphabetized account data. Assume all the accounts have normal balances.

Problem Ready B

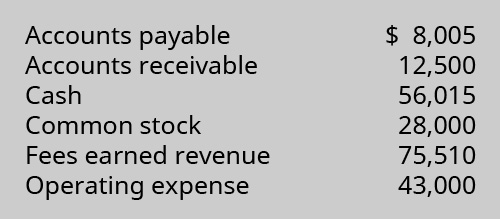

(Figure)Fix an unadjusted trial balance, in correct format, from the following alphabetized business relationship data. Assume all accounts have normal balances.

(Figure)Prepare an unadjusted trial residual, in correct format, from the following alphabetized account information. Assume all accounts accept normal balances.

Thought Provokers

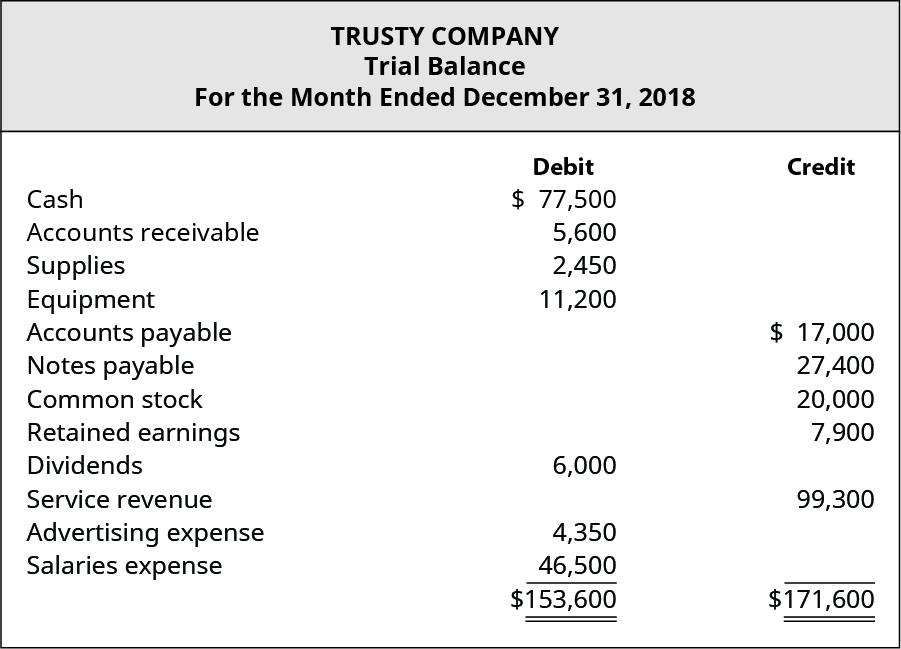

(Figure)Analyze Trusty Visitor's trial balance and the additional information provided to determine the post-obit:

- what is causing the trial balance to be out of residual

- any other errors that require corrections that are identified during your analysis

- the consequence (if any) that correcting the errors volition accept on the accounting equation

A review of transactions revealed the post-obit facts:

- A service fee of $18,000 was earned (only not withal nerveless) by the terminate of the period merely was accidentally not recorded as revenue at that time.

- A transposition error occurred when transferring the account balances from the ledger to the trial residual. Salaries expense should take been listed on the trial residuum as $64,500 only was inadvertently recorded as $46,500.

- Two machines that cost $ix,000 each were purchased on account only were not recorded in visitor accounting records.

Footnotes

- one James Titcomb. "Arthur Andersen Returns 12 Years after Enron Scandal." The Telegraph. September 2, 2014. https://world wide web.telegraph.co.united kingdom of great britain and northern ireland/finance/newsbysector/banksandfinance/11069713/Arthur-Andersen-returns-12-years-after-Enron-scandal.html

Glossary

- trial residue

- list of all accounts in the full general ledger that have nonzero balances

- unadjusted trial balance

- trial balance that includes accounts earlier they accept been adjusted

Source: https://opentextbc.ca/principlesofaccountingv1openstax/chapter/prepare-a-trial-balance/

0 Response to "How Do You Know Which Order to List Accounts on a Trial Balance"

Post a Comment